This is part 1 in a 3-part series on Trump Accounts. In summary, Trump Accounts are free money for...

At Virtus Wealth Management, your Southlake independent financial advisors, we help our clients prepare for a financially-secure future by developing long-term strategies that focus on the “big picture” versus short-term gain, thereby managing risk.

Today’s economic conditions and uncertain financial markets require the savvy investor to go beyond traditional boundaries.

Our mission is to provide innovative, sophisticated and highly customized wealth management solutions and financial advice that address all facets of your finances.

We tailor everything to each of our clients’ specific needs so that each client can pursue his or her different goals.

Virtus Wealth Management is the product of a 2016 merger between two well-established Texas wealth management firms.

Wealth management is more than just investment advice – it includes all aspects of a client’s financial life.

This is part 1 in a 3-part series on Trump Accounts. In summary, Trump Accounts are free money for...

This is the last article in our HSA series and goes into detail regarding strategies that could be...

Wealth management is more than just investment advice – it includes all aspects of a client’s financial life.

At Virtus Wealth Management, we believe we can help you no matter what age you are, what life stage you are in, or how much money you are working with. We want you to feel educated, empowered, and involved in the planning of your financial future.

When you retire, it’s nice to have income options, and focusing on building those income options is a sound part of a retirement plan. You are probably most of the way there, and you don’t even know it! Income options include tax-deferred income, tax-free income, and guaranteed income. Tax deferred income comes from your 401k and/or IRA accounts. Tax-free income comes from your Roth IRA.** Guaranteed income can come from an annuity, a pension, and/or Social Security.***

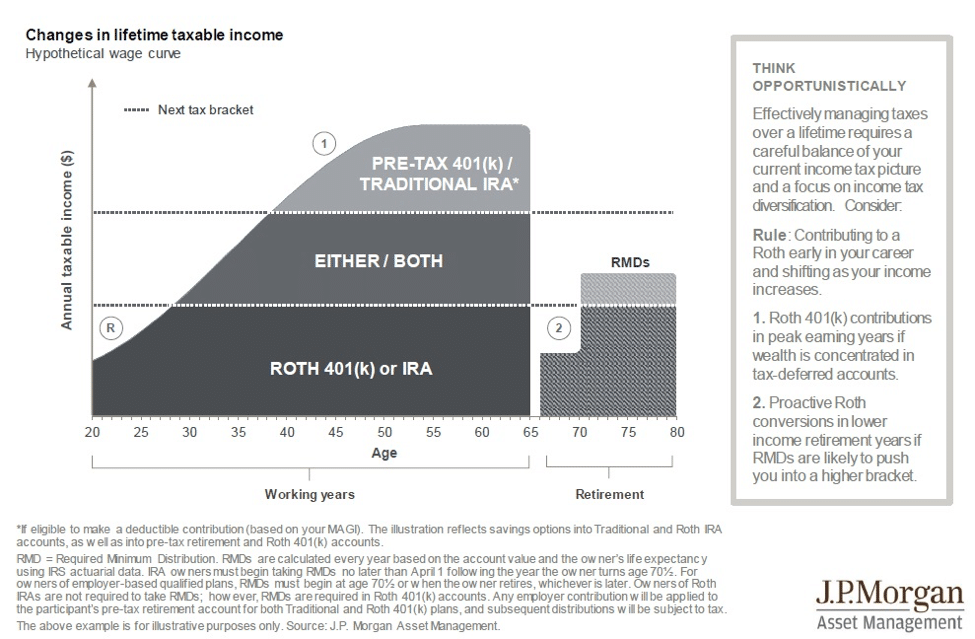

Effectively managing taxes over a lifetime requires a careful balance of your current income tax picture and a focus on income tax diversification. The answer to evaluating a Roth is to think opportunistically.

As a general rule, you should contribute to a Roth early in your career and shift to tax deferred vehicles as your income increases. This is represented by the circled R on the chart below. Over the years, as your income increases, if your wealth becomes concentrated in tax deferred accounts, you could direct funds to a Roth 401k (if it’s available to you). This is represented by the circled 1 on the chart below. Finally, as you reach your early retirement years, you could switch to proactive Roth conversions especially if your Required Minimum Distributions are likely to push you into a higher bracket. This is represented by the circled 2 on the chart below.

As you can see, managing your income options in retirement and tax planning go hand in hand, and we are here to help! Please contact us so that we can help you build your retirement income options.

Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual, nor intended to be a substitute for specific individualized tax advice. We suggest that you discuss your specific tax issues with a qualified tax advisor.

* Withdrawals from IRAs are subject to income taxes, and if made prior to age 59 1/2, a 10% penalty tax may apply

**The Roth IRA offers tax deferral on any earnings in the account. Withdrawals from the account may be tax free, as long as they are considered qualified. Limitations and restrictions may apply. Withdrawals prior to age 59 ½ or prior to the account being opened for 5 years, whichever is later, may result in a 10% IRS penalty tax. Future tax laws can change at any time and may impact the benefits of Roth IRAs. Their tax treatment may change. Traditional IRA account owners should consider the tax ramifications, age and income restrictions in regards to executing a conversion from a Traditional IRA to a Roth IRA. The converted amount is generally subject to income taxation.

***Annuity guarantees are based on the claims paying ability of the issuing company